2026 Outlook: Three Ways to Invest in China During the Year of the Fire Horse

Selfwealth

Key takeaways

The RBA increased the cash rate to 3.85% on 3 February, reflecting ongoing expectations that inflation is likely to remain above target for some time.

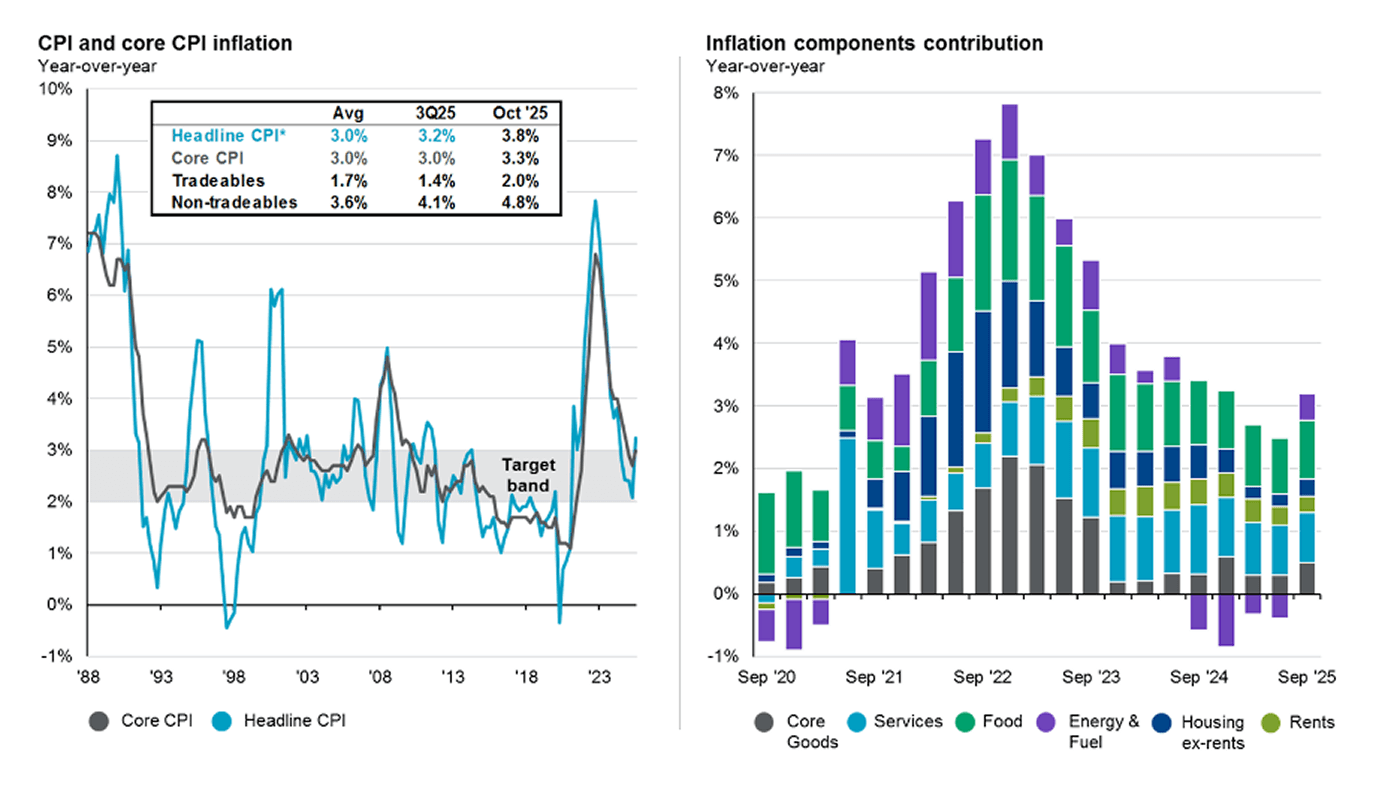

Inflation remains above the RBA’s 2–3% target band, with the annual Consumer Price Index (CPI) rising 3.8% in the 12 months to December 2025.

Higher interest rates affect sectors and companies unevenly, particularly those sensitive to borrowing costs or valuation changes.

For long-term investors, the focus shifts from predicting rate moves to understanding portfolio exposure in a higher-rate environment.

Why did the RBA increase rates?

Inflation is running hot. The CPI rose 3.8% in the 12 months to December 2025, remaining above the RBA’s 2-3% target range despite easing from earlier peaks.

Keeping prices stable is one of the most important jobs of the RBA – and it’s been a challenging task. But as the RBA governor pointed out this week, some of the drivers of high prices are beyond the central bank’s control. Global demand for commodities, domestic investments in AI and energy infrastructures, as well as fiscal spending, have all contributed to price momentum.

Image source: Livewire

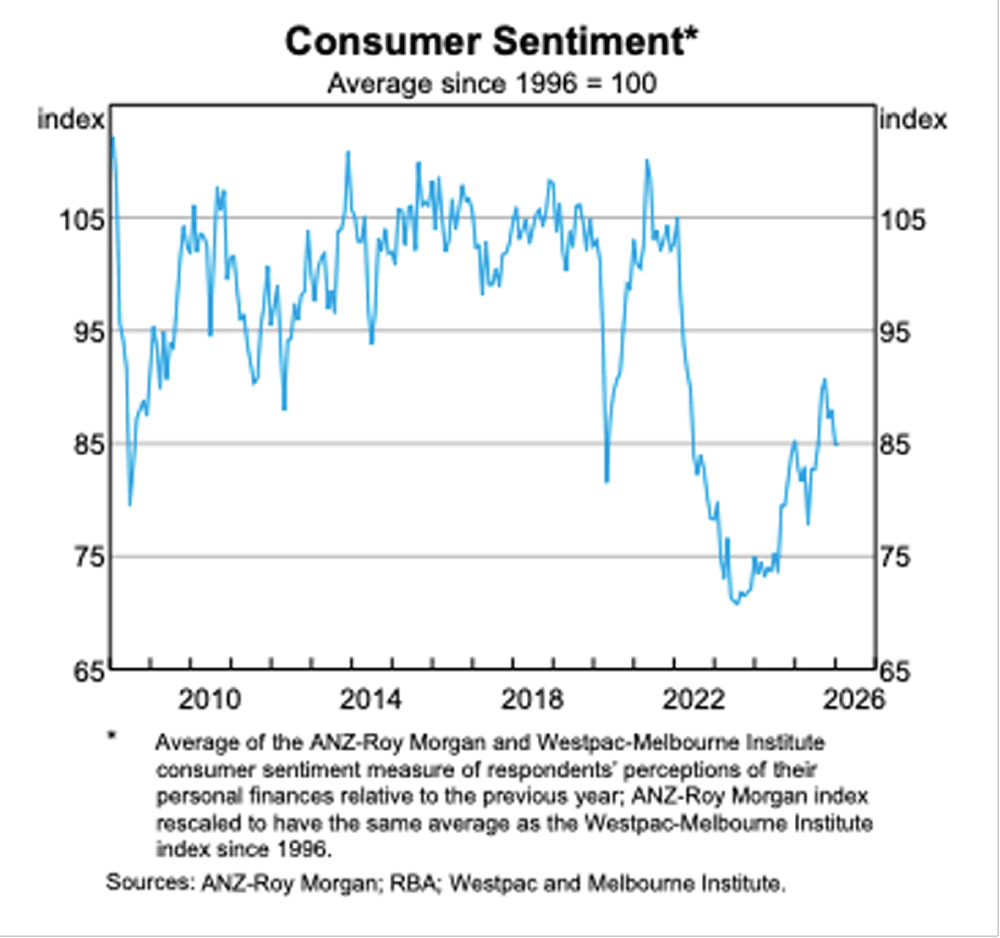

Consumer confidence is fickle. Households are feeling the pinch of higher financing costs. But recent remarks by policymakers suggest that “excessively high” inflation is the bigger threat to them, especially given the recent experience of post-pandemic price hikes. They also seem to believe financial conditions are not yet restrictive (i.e., there is more lending than needed).

This would give them room to hold or hike rates further. The quarter-point hike this month may not be the last this year. Markets are pricing in another 25 basis points of rate increases by August, according to the ASX’s RBA Rate Tracker.

Image source: J.P. Morgan Asset Management.

What does this mean for macro and markets?

In theory, higher interest rates are bad for businesses. The rate at which future cash flows are discounted rises, investors focus on profitability rather than future growth and financing becomes more costly as creditors grow cautious. Sectors like real estate, heavily influenced by interest rates, usually come under pressure.

But they are not inherently negative for equities. Hikes typically occur during economic expansions when corporate profits are rising. The ASX 200 rose, albeit modestly, during the 2022-23 rate hike cycle. The MSCI Australia Index also produced positive returns in 2023, albeit less than major global benchmarks.

The bigger threat is policy surprises. Markets would fret and sometimes rush to reprice their interest rate expectations. Mistakes by policymakers are also possible, for example, by misjudging credit conditions and tightening policy too much, hurting households, businesses, and ultimately growth in the economy.

Who Are The Winners and Losers?

Macquarie favours resources stocks during rate hike cycles as they benefit from stronger growth, provide inflation protection, and are less sensitive to rising bond yields, with basic materials and transport historically outperforming before the first RBA hike.

Conversely, the bank believes that cyclicals like media, retail, and discretionary sectors typically underperform as markets anticipate that the economy has reached its strongest growth phase and conditions will weaken ahead.

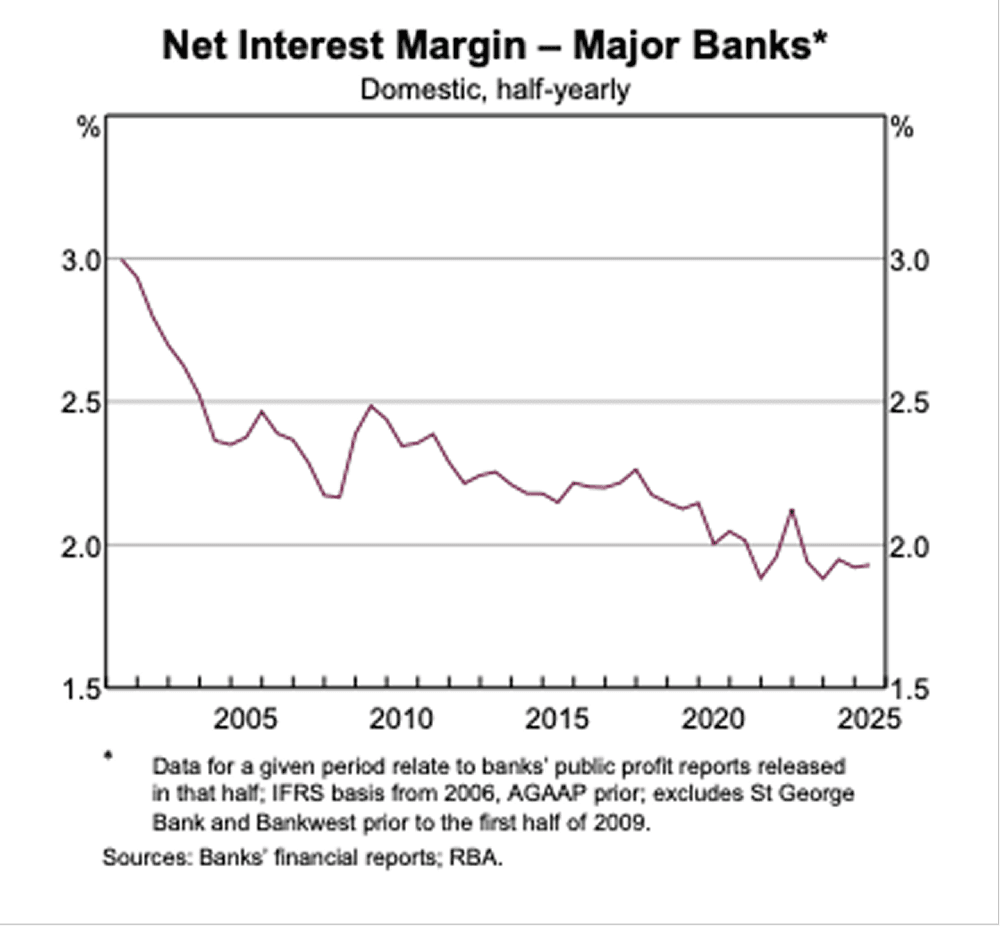

Typically, banks’ net interest margins would also expand in such an environment, although profitability could be challenged if growth slows meaningfully. The Aussie dollar has strengthened to a three-year high against the greenback as the interest rate differential between the two countries narrowed.

Image source: RBA

What Can I Do To Protect My Portfolio?

Diversification is essential. Recent market concentration in a few tech stocks in the US and the underperformance in Australian stocks have highlighted the need to look further afield and spread your bets across asset classes and regions.

Beyond Australian and US equities, Asian markets offer AI exposure through semiconductor manufacturers, while emerging markets look attractive with cheap valuations and a weakening US dollar. The recent “Takaichi Trade” also reminds us that the Japan reflation story has more room to run.

Gold continues to be a strong safe haven given ongoing geopolitical risks, and transition metals like copper offer long-term potential, despite near-term headwinds and volatility.

Let’s not forget that, while Australia is fighting inflation, many other markets are heading in the other direction. The Fed is still expected to deliver two rate cuts, as we discussed in our commentary last week, which would create a tailwind for USD bonds. Instruments like REITs, particularly in Singapore, could rise on lower financing costs and favourable local occupancy and rental rates.

You can learn more about diversification in this article.

A useful moment to reassess portfolio risk

Higher interest rates don’t automatically require portfolio changes. But they do create a natural checkpoint for investors.

Some questions worth asking include:

How dependent is my portfolio on a single economic outcome (strong growth, falling rates, rising property prices)?

Are multiple holdings exposed to the same underlying risk, even if they sit in different sectors?

Would higher rates for longer materially change the earnings outlook of my largest positions?

Often, the biggest risk revealed during rate cycles is concentration rather than market direction.

ETFs relevant to this article

ETFs can provide a simple way for investors to gain exposure to different regions, sectors, and asset classes without relying on individual stock selection. In a higher interest rate environment – where sectors and markets may perform differently – broad diversification can help investors manage concentration risk.

Below are examples of ETFs that investors commonly use to access areas discussed in this article. These are provided for illustrative purposes only and are not recommendations.

Broad Australian market exposure

Australian equities remain a core allocation for many local investors, particularly given exposure to banks, resources, and dividend-paying companies.

Examples include:

Vanguard Australian Shares Index ETF (ASX:VAS)

iShares Core S&P/ASX 200 ETF (ASX:IOZ)

BetaShares Australia 200 ETF (ASX:A200)

These ETFs provide diversified exposure to large Australian companies rather than relying on individual sectors or stocks.

International equities and global diversification

Higher-rate environments can affect countries differently. International ETFs allow investors to diversify beyond Australia and access global earnings growth.

Examples include:

Vanguard MSCI Index International Shares ETF (ASX:VGS)

iShares S&P 500 ETF (ASX:IVV)

BetaShares Nasdaq 100 ETF (ASX:NDQ)

Global ETFs provide exposure to international companies and sectors that may not be well represented in the Australian market.

Emerging markets and Asia exposure

As discussed earlier, some investors look to emerging markets or Asian economies for long-term growth exposure and diversification away from developed markets.

Examples include:

Vanguard FTSE Emerging Markets Shares ETF (ASX:VGE)

BetaShares Asia Technology Tigers ETF (ASX:ASIA)

These types of ETFs can provide exposure to regions benefiting from structural growth trends, although they may experience higher volatility.

Gold and commodities exposure

Gold and commodities are sometimes viewed as diversifiers during periods of inflation uncertainty or geopolitical risk.

Examples include:

Global X Physical Gold ETF (ASX:GOLD)

BetaShares Global Gold Miners ETF (ASX:MNRS)

Commodity-linked ETFs can behave differently to traditional equities, which is why some investors include them as part of a broader diversified allocation.

Bonds and income-focused exposure

Higher interest rates also change the outlook for fixed income. Bond ETFs may offer income and diversification benefits within a multi-asset portfolio.

Examples include:

iShares Core Composite Bond ETF (ASX:IAF)

Vanguard Global Aggregate Bond Index ETF (ASX:VBND)

Bond ETFs provide exposure to government and corporate bonds and may help balance equity risk within diversified portfolios.

Important disclaimer: SelfWealth Pty Ltd ABN 52 154 324 428 (“Selfwealth”) (AFSL 421789). The information contained on this website is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser and/or accountant. Taxation, legal and other matters referred to on this website are of a general nature only and should not be relied upon in place of appropriate professional advice. You should obtain the relevant Product Disclosure Statement for any product mentioned and consider its contents before making any decision.